- Popular Fintech

- Posts

- The many faces of Affirm

The many faces of Affirm

Affirm is more than just a point-of-sale lender. But what exactly are they?

Jevgenijs Kazanins

March 23, 2025 • Estimated Reading Time: 12 minutes

Hey!

Remember the phrase, “It’s a bird! It’s a plane! No, it’s Superman”? That’s what comes to my mind every time I think about Affirm. Is it simply an online lender with a smarter customer acquisition strategy? An up-and-coming credit card challenger? Or is it something else entirely - something we haven’t quite labeled yet?

Affirm has evolved a lot over the years. They started with a checkout button to help customers finance online purchases. Then went on to launch the Affirm Card, a new breed of cards that combines debit and credit capabilities. And now they want to power credit for all debit issuers out there.

But here’s what confuses me most: Affirm says it's “building a new kind of payment network.” Not a lending network. Not a commerce network. A payment network. That suggests Affirm’s ambitions might go far beyond what it is today.

Isn’t it exciting? Let’s dive in!

Jevgenijs

p.s. if you have feedback just reply to this email or ping me on X/Twitter

As a reminder, from now on, every other article will be available exclusively to premium subscribers. Consider upgrading to get full access and support my work:

Affirm as an online lender

Affirm $AFRM ( ▲ 3.29% ) used to be a pretty simple company. You could think of Affirm as an online consumer lender that has figured out a better way to acquire customers by integrating into the checkout process. Instead of getting a credit card or a personal loan, consumers could just use the Affirm button at checkout.

Yes, there was some complexity in the model, as some of the loans were interest-free, with merchants paying interest on behalf of the buyers through the merchant fees. However, the ZIRP era came to an end, and Affirm started originating more and more interest-bearing loans. At some point, one could have reasonably expected that interest-free loans would disappear altogether.

“…roughly 75% of our GMV coming from interest-bearing loans. Another 11% was coming from monthly 0% loans to consumers that were 3 months or longer in terms of the loan term. And then we were about 14% Pay in 4.”

So one can think of the reported “Gross Merchandise Volume” as lending origination volume, and the rest would be the same as for a consumer lender: interest income, cost of funding, credit losses, etc. Nothing unusual, a straightforward business model with several comparable companies.

Affirm as a neobank

However, things got more complicated over time. In 2022, Affirm crossed the 10 million active customer milestone. Then, in 2023, it crossed the 15 million active customer milestone. And this made me think: what if Affirm will eventually become a neobank? Nubank started with a credit card, perhaps, BNPL was an equally viable path?

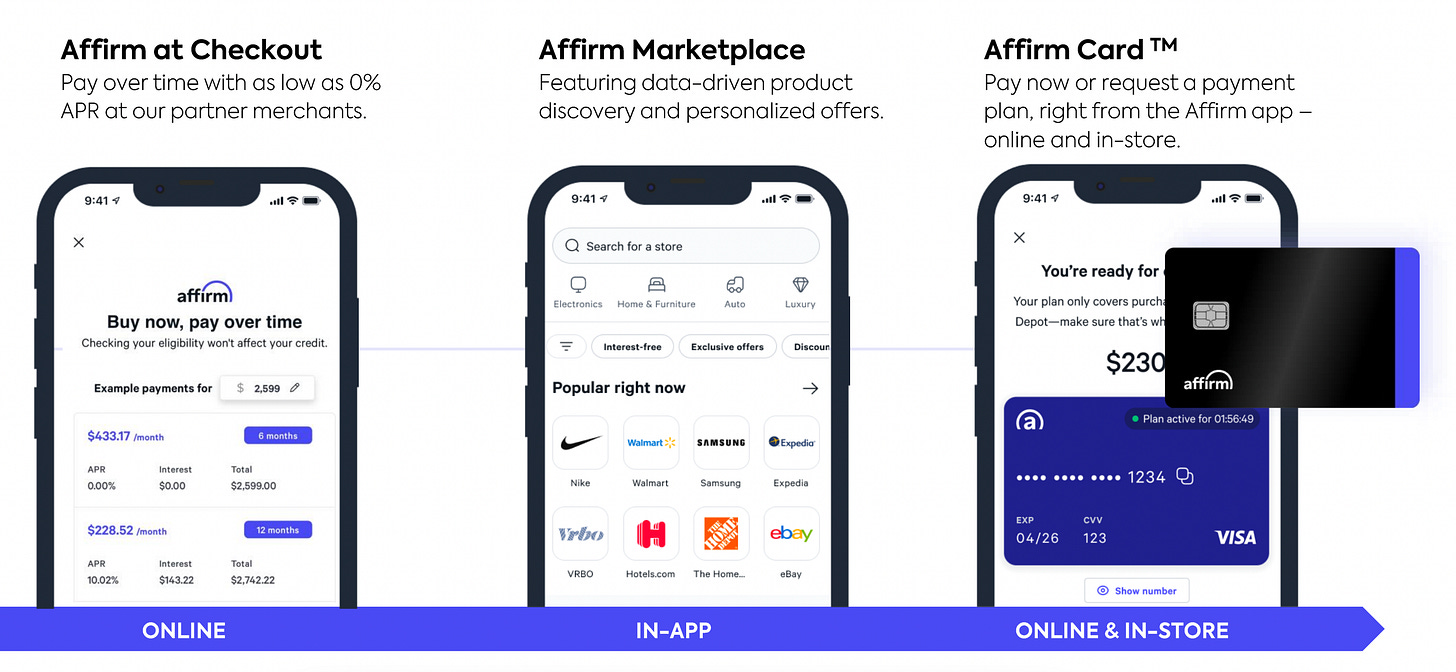

Around that time, Affirm became more vocal about its debit card, the Affirm Card, and about its intentions to expand into in-store commerce. Bear in mind, that back then, the Affirm Card seems like a regular debit card (more on this later). So it felt like Affirm started expanding beyond online lending.

Image source: Affirm Investor Forum 2023

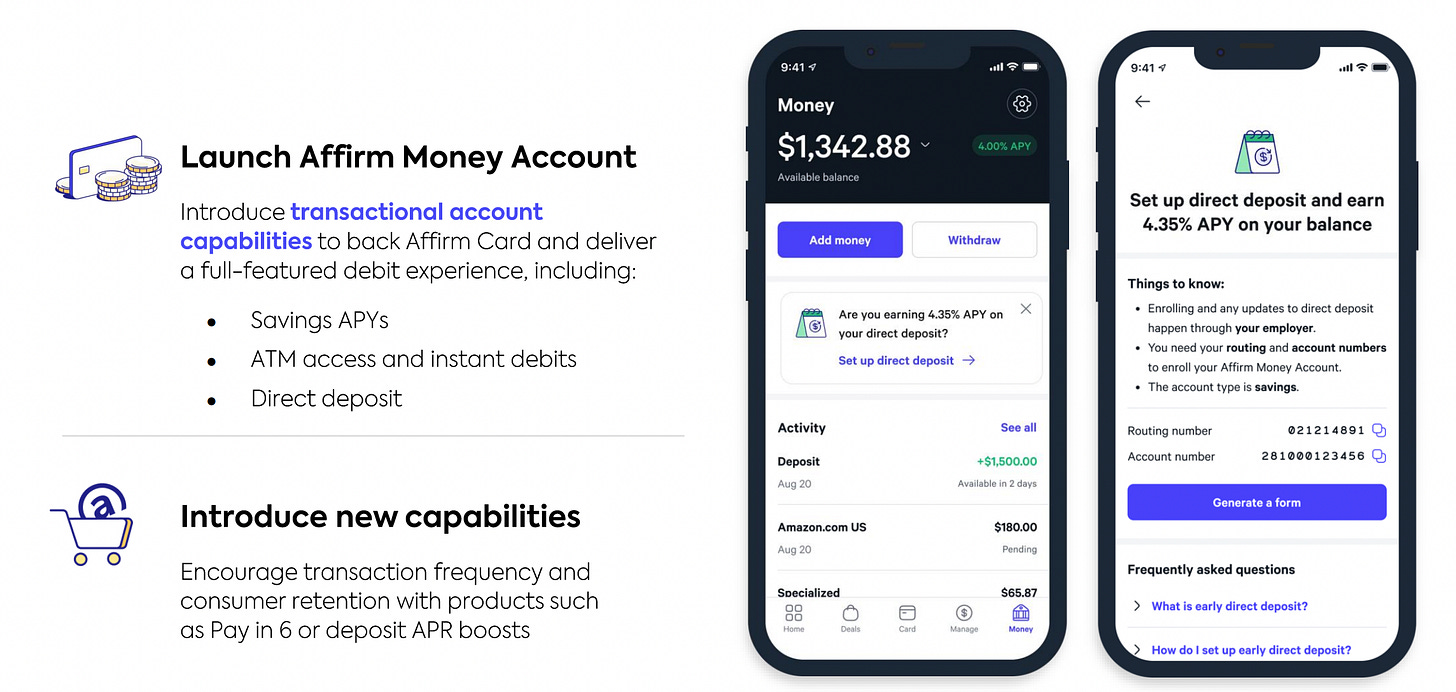

Then, in November 2023, at the Investor Forum, Affirm launched the Affirm Money Account, a high-yield “savings account with the flexibility of a checking account”. The way it was presented, and the features that it had (and still has), made it a viable alternative for a bank account.

Image source: Affirm Investor Forum 2023

“We're announcing the launch of Affirm Account, which is a transactional account with savings APY. Like any transactional account, it has an ATM access, direct deposit, all the things that you would expect with savings APY. And it creates a tighter experience with the Affirm Card.”

And just like that, at least in my head, Affirm stopped being simply an online lender and became a more complex creature. Affirm became similar to Cash App. Or rather an alternative version of Cash App, which actually managed to integrate Afterpay.

Affirm as the next-generation Amex

And then…Visa announced Visa Flexible Credential, a new type of card that combines the debit and credit capabilities under the same card. Visa Flex lets consumers choose how they want to pay for a purchase—whether from a linked checking account or a credit line.

Image source: Visa

And it turned out, that there was nothing “regular” about the Affirm Card. The Affirm Card was a real-life example of a Visa Flex card that combined debit and credit capabilities. Affirm customers can use Affirm Card as a debit card, but they can also fund their purchases with installment loans.

Image source: Affirm

“We're definitely not surprised by [ Visa announcement ]. We are the first card, I think, that's going to be a Flex card. If anybody has received an updated Affirm card, we have a new look to the card. If you've received it recently, you'll see Flex on the back. So we're shipping Flex cards today.”

For a while, I had a thesis that Affirm should be compared to American Express. Both companies are payment networks, and both are lenders too. After all, Amex’s executives have been saying for a while now that the company’s loan book grows primarily from a BNPL-like product.

However, the element of a card was missing…and the Affirm Card (put on Visa Flex rails) completed this puzzle. At the end of 2024, there were 1.7 million active Affirm Card users, and Affirm disclosed an internal goal of 20 million cards (without specifying when). American Express has 46.3 million cards issued to U.S. consumers.

Image source: Affirm FY Q2 2025 Earnings Supplement

“…we've set the milestone internally to get to 20 million active cardholders…we've set a target of getting to $7,500 per user per year for the frequency, too.”

This made me drop the idea of Affirm becoming a neobank. American Express also offers savings accounts, but these serve solely as a funding source—not as part of a broader goal to become a primary bank for its cardholders. Thus, I started living with the idea that Affirm could become the American Express for the next generation of consumers.

“…we really are focused on the over $1 trillion of credit card debt that is outstanding with U.S. consumers. We think we have a competitive advantage with the way that we build our underwriting models, and we can do that in the unsecured space as well as anyone. And so we're going to be heads down and focused on what is undeniably an enormous opportunity in the U.S. and also internationally.”

Affirm as an embedded lender

…and then, Affirm announced a partnership with FIS to provide credit capabilities to FIS’s debit card issuer clients. Essentially, any bank can issue Visa Flex cards, and Affirm is ready to provide credit for such debit issuers. The issuer gets higher interchange, Affirm gets to earn the interest…a win-win.

“FIS debit processing bank clients will be able to integrate Affirm’s pay-over-time solution directly into their existing debit card program via their digital banking and mobile app platforms”

However, this new direction completely broke my thesis of Affirm becoming the next Amex, because Amex does not power credit for other debit card issuers! This is some kind of embedded lending play!

Moreover, after giving it more thought, I realized that Affirm has been playing this embedded lending game for a while now. Shopify’s Shop Pay Installments are powered by Affirm. Oh, and Apple has embedded Affirm into Apple Pay!

Image source: Affirm

"Affirm’s premier technology, world-class team, and commitment to transparency make them a natural fit to continue supporting merchants in the Shopify ecosystem, and we look forward to bringing this same value to our merchants in Canada, the U.K., and beyond.”

So…Affirm is a point-of-sale lender via its checkout button. Affirm is a new-generation credit card company via the Affirm Card. And now they are also an embedded consumer lender. I mean can you name any company that would do all of the above?

“…we want to be available at all of those touch points. And we have plenty of places where we're available with a direct integration at the merchant, through Shop Pay, through our own card, through Apple Pay, like being available through all the different touch points creates an incremental opportunities.”

Affirm as a payments company

But what confused me the most is… You know how every press release has that “About X” section at the end? In those “about" sections, Affirm says “Affirm’s mission is to deliver honest financial products that improve lives. By building a new kind of payment network…” Not a lending network, not a commerce network, a payment network!

“Affirm’s mission is to deliver honest financial products that improve lives. By building a new kind of payment network – one based on trust, transparency and putting people first – we empower millions of consumers to spend and save responsibly, and give thousands of businesses the tools to fuel growth.”

…and during their Investor Day in 2023, Affirm management showed this slide 👇🏻 “Five years from now…the leader in payments”. What is this about?! Will Affirm eventually go after Visa and Mastercard or something?

Image source: Affirm Investor Forum 2023

So who are you, dear Affirm?! I am definitely excited to find out!

Cover image source: Affirm

Disclaimer: Information contained in this newsletter is intended for educational and informational purposes only and should not be considered financial advice. You should do your own research or seek professional advice before making any investment decisions. Read the full disclaimer here.